States use different methods to estimate how much revenue they will have available to spend in future years. States that do not produce timely or detailed revenue estimates may experience unexpected deficit shocks or contribute insufficient resources to their state budget stabilization fund to weather downturns in future years. Recent recommendations to improve forecasting include measures for transparency, independence, and multistakeholder inclusion. 1

Revenue forecasts can be produced by the executive branch or legislative branch or they can be outsourced to academics or economic consultants. In 2015, 31 states and the District of Columbia had a formal revenue estimating group. In eight states, the executive budget agency was solely responsible for preparing the revenue forecast for the governor’s budget; in another eight, an independent board or commission was responsible. In 28 states, multiple agents were involved in preparing the governor’s forecast, including in some cases the governor’s office itself or the legislature. Half of all states use consensus forecasting.

In some states, the executive and legislative branches produce competing forecasts. In Colorado, for example, both the executive Office of State Planning and Budgeting and the Legislative Council produce separate revenue forecasts that the Joint Budget Committee chooses between when balancing the budget.

A 2013 study examining state revenue forecasts from 1987 to 2008 found that

Although some states centralize forecasting responsibility with the executive branch budget office, others employ a multibranch, consensus-based process.

Twenty-five states used a consensus forecasting process in 2015, which involves formally garnering participation from many budget stakeholders across several executive and legislative government agencies.

In Massachusetts, the executive budget office develops the budget collaboratively with the legislature. The state also holds annual consensus revenue hearings, which are chaired by leadership in the executive budget agency as well as the house and senate budget committees. During the hearings, the executive and legislative leadership hear testimony from budget experts and economists regarding revenue projections and adjust accordingly. 2

Although the consensus process has been popularly touted as a way to reduce forecasting errors, one 2011 study did not find a clear link between consensus forecasting and accuracy.

Forecasting errors are more likely to be caused by a recession and to occur in smaller states that rely heavily on revenues from only a few sectors of the economy or specific revenue instruments. Alaska, for example, relies heavily on volatile revenue from natural resource extraction.

Accuracy, however, may not be the only outcome of interest. Even if research is unclear on whether consensus forecasting reduces errors, researchers praise its ability to “smooth” the budget process by depoliticizing revenue estimation and ensuring that everyone has agreed to the same numbers. A case study of Indiana suggested that the accuracy of revenue estimates is less important than whether the estimates are accepted by all the stakeholders who will ultimately use them.

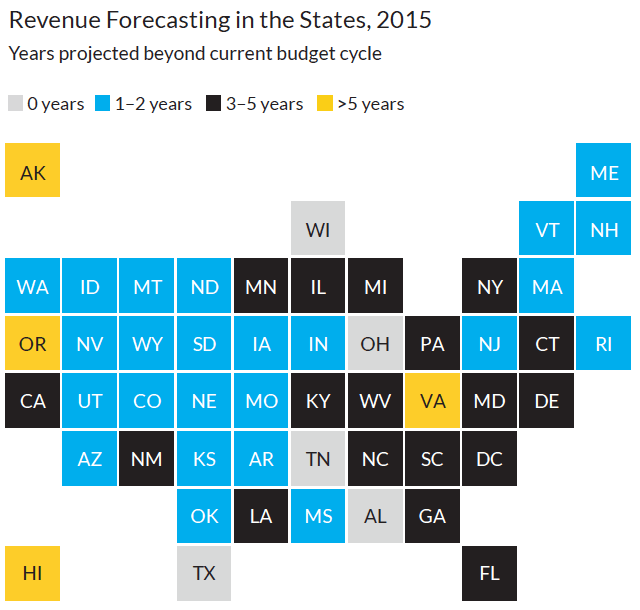

On average, states produce revenue forecasts for two to three fiscal years beyond the current budget cycle. Some states, such as Alaska, provide long-term revenue forecasts for up to 10 years beyond the budget year; many produce a revenue forecast for only the current budget cycle. Twenty-nine states forecast revenues for less than three years beyond the budget cycle.

“The whole (consensus forecast) system is designed to be as transparent as it possibly can so you end up with a single consensus forecast.”

– John L. Mikesell, Chancellor’s Professor Emeritus, Indiana University Bloomington 3

Source: National Association of State Budget Officers, Budget Processes in the States (Washington, DC: National Association of State Budget Officers, 2015).

Note: NASBO did not report revenue forecasting timeline for North Dakota in 2015; figure uses information authors obtained directly from the state.

1 For more information, see Megan Randall and Kim Rueben, Sustainable Budgeting in the States: Evidence on State Budget Institutions and Practices (Washington, DC: Urban Institute, 2017).

2 National Association of State Budget Officers, Budget Processes in the States (Washington, DC: National Association of State Budget Officers, 2015).

3 Donald J. Boyd, Lucy Dadayan, and Robert B. Ward, States’ Revenue Estimating: Cracks in the Crystal Ball (Washington, DC: Pew Charitable Trusts, 2011), 32.

To reuse content from the Tax Policy Center, visit copyright.com, search for the publications, choose from a list of licenses, and complete the transaction.